Last month I wrote an article questioning the logic behind closing down the U.S. economy, and looking at the full social and economic costs associated with our social distancing policies. Needless to say, while there were strong opinions expressed on both sides of this debate, more people opposed my conclusions. They believed that the shutdown should have been pursued at all costs, whatever that means. As a result this article will attempt to quantify some of those costs, and present an alternative option that could possibly have achieved the best of all worlds. It does not attempt to re-litigate the issue of whether we should have made the wholesale decision to close down the economy. That decision is already made. The best we can do now is evaluate the consequence of that decision.

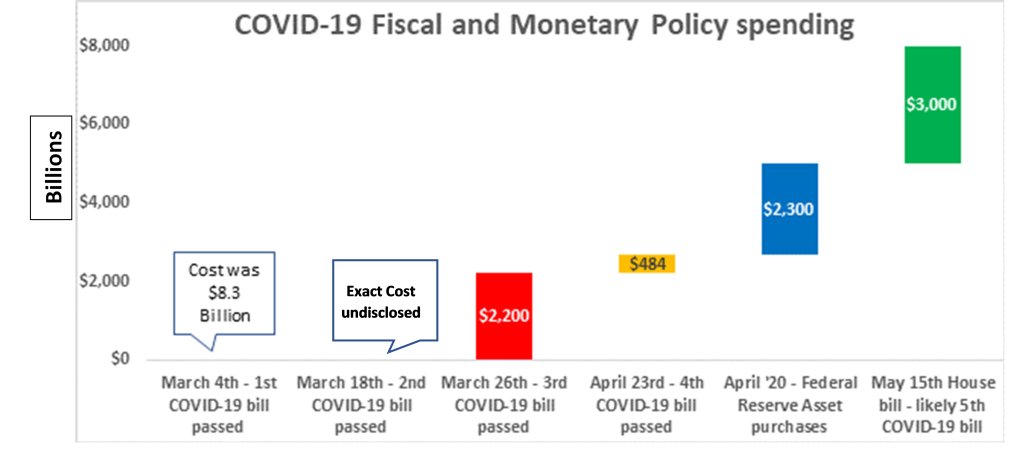

On May 15th the House of Representatives passed a $3 Trillion coronavirus relief bill intended to provide assistance to state and local governments, hazard pay to frontline health care workers, student debt forgiveness and bolster the Medicaid and Medicare health programs. The Senate, interestingly has not yet acted upon this House bill, preferring instead to propose its own new package. This $3 Trillion proposal is expected to be in addition to the $2.2 Trillion rescue and recovery package that the Congress already passed on March 26th to stimulate demand and promote economic growth, the third such measure to deal with the COVID-19 pandemic. Incidentally one month after that initial March 26th recovery package Congress approved another $484 billion coronavirus rescue package on April 23rd that was intended to deliver emergency aid to small businesses and hospitals because well two trillion dollars was just not sufficient. That means between the Executive and Legislative branches–that control fiscal policy–in just a month they had committed nearly $2.7 Trillion to clean up the mess caused by shuttering the economy, and are negotiating to spend another $3 Trillion. But exactly where does the government get all of this money to be spending like that? Do they have it stored up in a vault somewhere just saving for another emergency situation like this? Or are they relying on their good faith and credit to expand our already burgeoning National Debt beyond its already stratospheric $25,481,800,000,000 levels (read that twenty-five Trillion, four hundred eighty-one Billion, eight hundred million dollars) as of noon ET on Memorial Day. [It is important to note that this twenty-five plus Trillion dollar Debt figure significantly understates the true financial obligation of the Federal Government. When we add in the Government’s lifetime obligations to pay Medicare and Social Security benefits to its citizens, and military & civilian retirement commitments to its employees the Truth in Accounting nonprofit organization estimates that the Federal Government’s true financial obligation is closer to one hundred and seventeen Trillion dollars.]

Not to be outdone by our fiscal policy authorities, the ‘experts’ on the monetary policy side–the Federal Reserve–also contributed to the economic stimulus during the first week of April by purchasing over $2.3 Trillion of Bonds and other securities. They expanded their Balance Sheet by increasing the total assets base from $870 Billion in August 2007 (just before the great recession) to a whopping $6.37 Trillion in April 2020, and they did this just by writing a check to buy these assets, in effect ‘printing new money’. According to the Federal Reserve it will make an open-ended commitment to launch a barrage of programs that keeps buying assets under its quantitative easing measures. These include:

• a commitment to continue its asset purchasing program “in the amounts needed to support smooth market functioning and effective transmission of monetary policy to broader financial conditions and the economy.”

• purchase of agency commercial mortgage-backed securities as part of an expansion in its asset purchases. This represents an expansion into the commercial sector of real estate for the central bank’s acquisitions.

• purchasing the investment-grade corporate bond securities in primary and secondary markets and through exchange-traded funds.

• an unspecified lending program for Main Street businesses and the Term Asset-Backed Loan Facility implemented during the financial crisis.

• a program worth $300 billion “supporting the flow of credit” to employers, consumers and businesses and

• two facilities set up to provide credit to large employers.

In just over one month America’s economic policy-makers (on both the fiscal and monetary sides) have borrowed over $5 Trillion to resuscitate the economy, hoping for a ‘bank-shot’ recovery with promises of more to come. Five Trillion dollars is a lot of money, and something that most of us cannot even fathom. Therefore to put that spending into context let’s compare it to the GDP of every country in the world. That level of spending represents the total value of all goods and services produced within the U.S. economy within any three-month period in 2018. It also represents the total value of all production within every country in 2019 except the United States, China and Japan. In the case of Japan five Trillion dollars would represent their total GDP for eleven and a half months in 2019. Adding an extra $3 Trillion to that number would make this round of spending the third largest economy in the world if it was its own country, such is the magnitude of these unprecedented spending levels. No matter how you look at it, it’s an incredibly large number indeed. But just how well are these programs expected to work, and how will they be repaid.

The Congress and the White House are relying on Keynesian-style fiscal policies similar to the ones used to stimulate the economies of America and Western Europe after World War 2. Those spending plans had a huge multiplier effect that stimulated their respective economies. That in turn caused private sector industries to thrive, thus reducing the role of the governments in the succeeding years. Owing to the relatively lower debt levels then in effect that policy was able to work. However, in 2020 with the U.S. already owing more than its total GDP there is very little opportunity for future stimulus should the next crisis occur within the next few years. The fact is that the country has a looming Medicare crisis with the hospital insurance trust fund expected to run out of money in 2026, and a pending Social Security one expected in 2034, therefore it is clear that this $5 Trillion infusion brings with it enormous Opportunity Costs as it will affect our ability to address those and future crises.

To underscore this let’s break down how debt-financing works. When someone spends out of their current income they have all of their future income available to spend in the succeeding years. However, when we use debt-financing we are spending out of future income. That means the five Trillion dollars that we spend today (in addition to the twenty-five plus Trillion dollars we owed before) will be coming from income expected to be earned in future years. Not only will we have to find additional funds to take care of Medicare and Social Security obligations, but we will also need to do it with less resources as we’ll have a larger debt load to repay.

Consider this, at the end of 2019–including interest on the Debt held by the public and Debt held by government accounts aka “intragovernmental debt”–the Federal Government paid approximately $570 Billion in interest payments, representing over 16 percent of all Tax receipts. That is about 1 in every 6 dollars received going out to pay interest on the Debt. This number is despite historically low interest rates in 2019 and 2020. However, in 10 to 20 years when these existing Debts mature and new ones have to be issued to replace them the Federal Government would have to pay significantly higher interest rates on much higher Debt levels. As a result the Congressional Budget Office estimated that Net Interest Payments will exceed $1 Trillion by 2030. This means that in the future for every $1 in tax revenues that the Federal government collects it will most likely have to divert between 20 and 25 percent just to pay the interest on that Debt, that is nearly 1 in every 4 dollars. The consequence of all this is that less than 80 or so cents on every dollar will be available for all other Federal government obligations and future commitments, unless of course the government continues to borrow more.

The issue with debt-financing is that it will have to be repaid at some time in the future. It therefore comes with a price. It borrows from the future to spend in the present. The expectation is that future generations will need to sacrificially repay those loans for the benefit of the present generation, and they will do so with fewer educational resources committed to them and reduced employment prospects available to them today.

As Senate Majority Leader McConnell and his Republican colleagues contemplate another round of Trillion dollar fiscal policy support to compete with the three Trillion dollar proposal from Speaker Pelosi and her House colleagues it is imperative that they carefully weigh the present-day benefits of any new spending plans against the long-term costs to future generations associated with the additional Debt burden. This is not free money. It will be incumbent upon our children and their children to repay it therefore give them a say in how much we should borrow, and how we should spend it.

Keith Thompson is a former Senior Economist with an agency within the U.S. Department of the Treasury, and a former adjunct Economics professor with Ramapo College of New Jersey. He currently works as an international tax professional for one of America’s largest corporations.