As we close out the year 2016 it is an opportune time to reflect on the state of the American Union and the pathway forward for sustained growth. After one of the most contentious presidential elections in modern political history America is once again juxtaposed in that delicate nexus between hope and disillusionment. Hope resonates amongst the supporters of President-elect Trump who see optimism in the country’s future, whereas despair looms large over the supporters of Hillary Rodham Clinton who worry about an America very different from the one they envision. Yet all Americans, Democrats and Republicans alike, should show some measure of concern for our youth who were largely left out of the electioneering discourse about the country’s future.

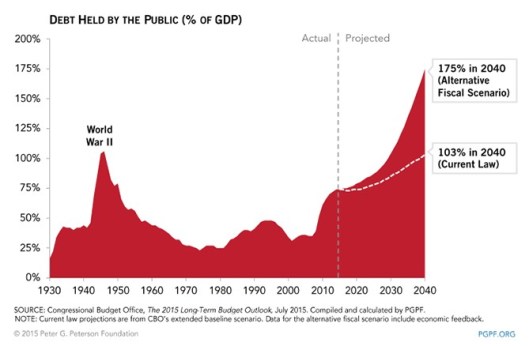

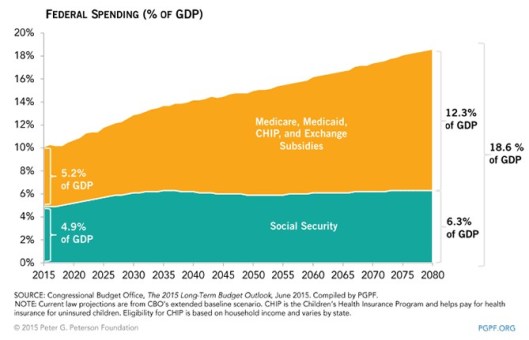

Let’s consider that the country’s largest economic constraints – the overburdened National Debt, soaring Social Security costs, and out-of-control Medicare obligations – represent the Federal government’s largest fiscal outlays. We are at a period in our history where Debt to GDP (including intra-agency Debt) is now over 100%, Social Security expenditures are running at nearly $900 Billion last year (23% of the Budget), and net Medicare/Medicaid obligations are currently at over $580 Billion in 2016 (15% of the Budget). What’s more troubling, however, is the trend in these numbers. The Peterson Foundation, with data from the non-partisan Congressional Budget Office (CBO), estimates that under existing law each will grow exponentially over the next 20+ years. Yet despite that impending fiscal crisis precious little was discussed about either long-term obligation on the campaign trails. Who does America think will be left to clean up the financial mess from these out-of-control spending, our youth. That would be the many of us currently in middle age, our young children and our (eventual) grand-children.

Let’s consider that the country’s largest economic constraints – the overburdened National Debt, soaring Social Security costs, and out-of-control Medicare obligations – represent the Federal government’s largest fiscal outlays. We are at a period in our history where Debt to GDP (including intra-agency Debt) is now over 100%, Social Security expenditures are running at nearly $900 Billion last year (23% of the Budget), and net Medicare/Medicaid obligations are currently at over $580 Billion in 2016 (15% of the Budget). What’s more troubling, however, is the trend in these numbers. The Peterson Foundation, with data from the non-partisan Congressional Budget Office (CBO), estimates that under existing law each will grow exponentially over the next 20+ years. Yet despite that impending fiscal crisis precious little was discussed about either long-term obligation on the campaign trails. Who does America think will be left to clean up the financial mess from these out-of-control spending, our youth. That would be the many of us currently in middle age, our young children and our (eventual) grand-children.

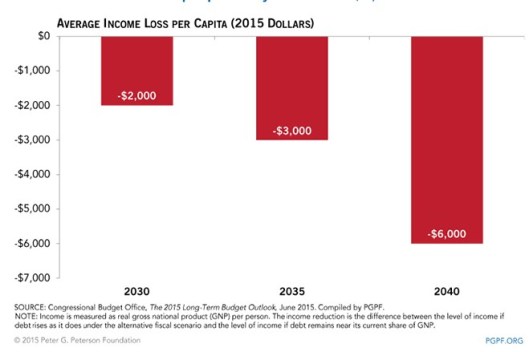

Now that the semester is over I have time to reflect on the happenings in my College economics classes. At the end of a recent class a student came up to me to discuss the state of the economy. “Why” he asked “does our government make decisions where the costs of those decisions do not fall on the same group of people who receive the benefits.” That was a hard one to answer, I responded. After all politicians seem to be incentivized to make decisions with short-term benefits (so that they can effectively stay in power) hence it is rational for them to implement policies that benefit population groups with the highest voting rates (and that coincidentally does not belong to Millennials who had just a 50% voter turnout in the recent election). Conversely, tough decisions that have primarily long-term benefits tend to be postponed (or in Washington speak they “kick the can down the road”). That is the current state of our National Debt, Social Security, and Medicare obligations. The consequence of these decisions is that the living standards and income of our youth will significantly decline in the years ahead as the Peterson Foundation chart below shows.

It is time that our politicians start actively thinking about the next generation when they craft policies. America can’t keep spending just to please the current generation of retirees with little regard for the well-being of our youth. After all it is America’s youth who will have to pay for these obligations in the years to come in the form of higher taxes, reduced benefits & services and lower real incomes.

President-elect Trump’s new administration and Congress need to put a plan in place to deal with these impending calamities, specifically:

- Limit the Debt to GDP ratio to no more than 100%, with a plan to pay it down annually.

- Limit the Overall Spending to GDP ratio to no more than 20%.

- Limit the Budget Deficit to GDP ratio to no more than 1%.

- Finally, both groups need to institute a super-majority requirement in both houses of Congress that must be met before these ratios can be breached (and only in cases of National emergencies).

The longer-term policy goal should be to get America’s fiscal house in order by generating Budget Surpluses and using them to pay down the Debt. If we don’t act now our youth will inherit an economy that looks a lot closer to a Third World economy, than the Advanced Industrial power that it truly is.

Keith Thompson is a Senior Economist in Transfer Pricing with an agency within the U.S. Department of the Treasury, and an adjunct Economics professor with Ramapo College of New Jersey.